The Global Games Investment Review for Q3 2014 from Digi-Capital has been released, and it shows some important trends in the gaming industry. Tim Merel, managing director of Digi-Capital, noted the report’s highlights:

- Megadeals drove $12.2 billion in games acquisitions to Q3 2014, already doubling full year 2013;

- There were five “billion dollar” deals (Mojang, Oculus, Giant Interactive, Twitch, FunPlus);

- American (five) and Chinese (five) buyers dominated the top 10 acquisitions to Q3 2014, a major shift from Asian buyers taking 9/10 in 2013 and 8/10 in 2014; and

- Games investment returns skyrocketed to>11x to Q3 2014.

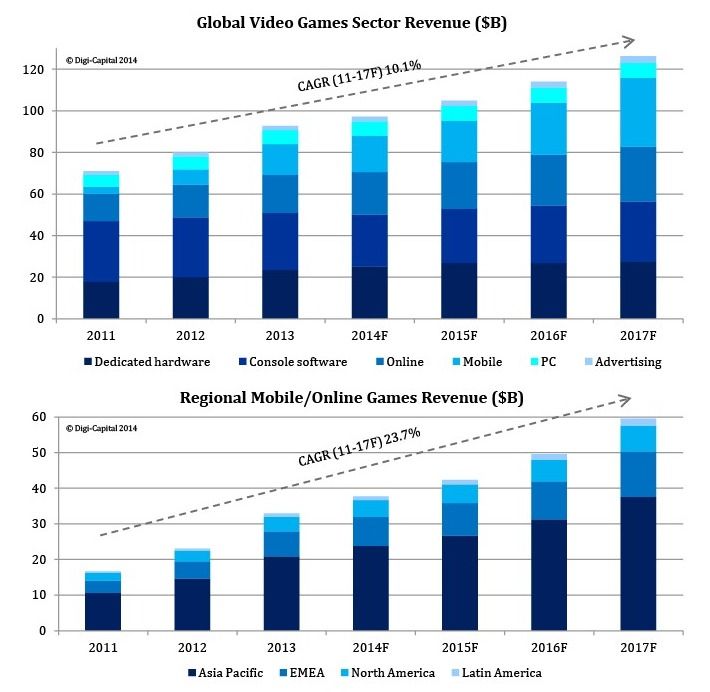

Digi-capital sees the total game software revenues worldwide reaching $100 billion annually by 2017, with the main driver being mobile games. The mobile game business could grow to $60 billion by 2017, which is a compound annual growth rate averaging 23.7 percent between 2011 and 2017. Meanwhile, Digi-capital sees console game revenue staying relatively flat, with the increasing sales of the latest consoles managing to offset the decline in older consoles but not exhibit much growth.

This is disheartening news, but it goes along with the general view of analysts in the game industry. We haven’t heard much about this lately, but if you think back about a year or so many game company execs were excited by the prospects of new consoles. Of course, everyone who had a stake in the success of new consoles was inclined to be as positive as possible, because for the most part new console purchases are about the customer’s belief that over time, the number of cool games this new hardware lets them play will be worth the cost of the hardware.

Still, one year in to the latest generation of consoles, it’s not entirely clear where we will end up overall. Sales of both the PS4 and the Xbox One continue to outpace their predecessors, yet sales of software for those consoles is still soft. Part of that can be attributed to tracking issues, because an increasing percentage of games (10 to 15 percent according to some publishers) are being sold digitally rather than in retail stores. Yet tracking of digital sales is getting better, and we don’t see a huge surge in sales there.

Publishers are getting by with increasing amounts of DLC for all titles, driving up the revenue (and, effectively, becoming a price increase that you can elect to take or not). Still, the increasing quantity of DLC has a downside as well — it keeps players engaged with a game for far longer, thus reducing the desire to buy the latest version of the game. This is clearly illustrated by Sterne Agee’s projection that the upcoming Call of Duty: Advanced Warfare will sell only 17 million copies, 15 percent less than the 20 million unit sales of last year’s Call of Duty: Ghosts. Which, in turn, is less than the sales of the previous version of Call of Duty.

This slide in the sales of the latest version of the top franchise for Activision has worrisome implications for all publishers. It’s not that Activision isn’t putting enough resource into it — the company now has three studios working on the franchise, giving each one three years to produce the latest version. The issue really is a result of two factors: The drive to give the top franchises a yearly major release (essentially, a new game), and the now obligatory DLC that appears every month or two. Those factors, combined with the increasing importance of multiplayer play, mean that players have less desire to shell out $60 for a new game that may or may not be as much fun as the older version they are currently playing.

It’s no wonder, then, the game publishers are turning towards faster growing markets. Even Blizzard, famously focused on PCs, has been finding success first on consoles (with Diablo III) and on tablets (with Hearthstone doing amazingly well for them). Now Blizzard’s opened up to possibilities on mobile, so we can probably expect more mobile ventures in the future. It will be interesting to see how well Activision does the Skylanders: Trap Team on tablets, which marks the first time the franchise has exactly the same content on tablets as it does on consoles — and at the same price point, too.

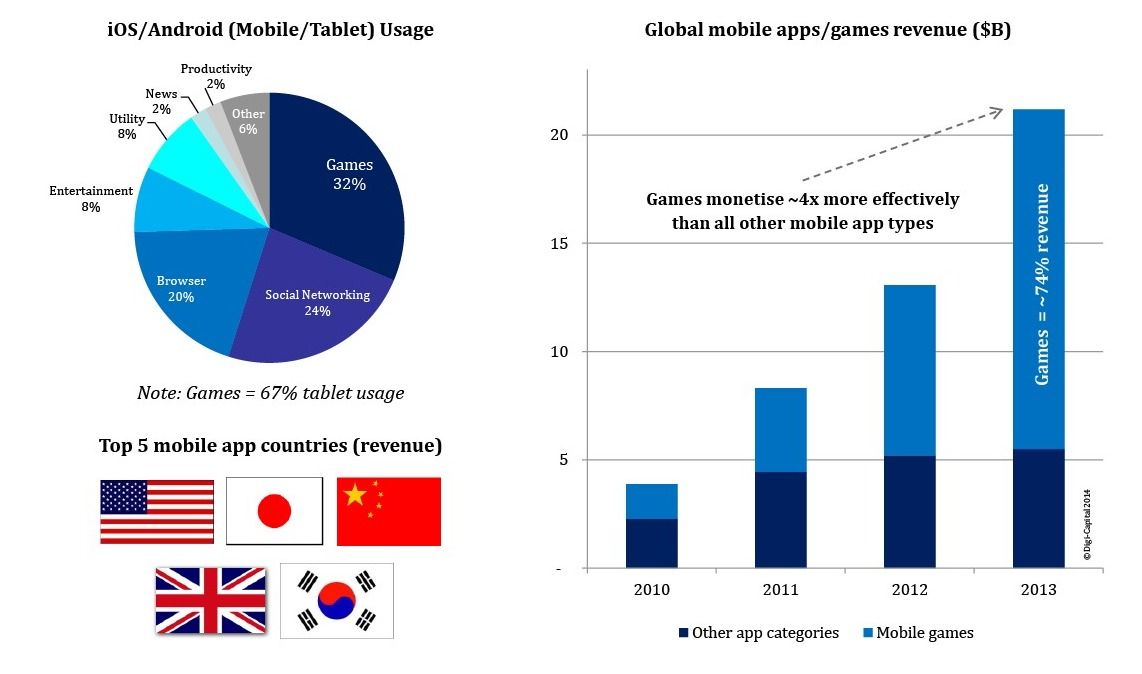

Mobile is clearly the best overall growth market for games on a global basis, and any major game company is going to want to have a piece of that action. The Digi-Capital report shows how important games are to the overall mobile app ecosystem, with games reponsible for by far the largest revenue share out of all types of apps — 74 percent of app revenues come from games. More than that, games handily beat even social networking apps for the amount of time spent, with 32 percent of all time spent on smartphone apps being devoted to games, with social networking coming in second at 24 percent. On tablets, the amount of time devoted to games is a staggering 67 percent. It’s easy to see why some people are calling tablets “the new gaming console.”

Digi-Capital also noted the record mergers and acquisitions (M&A) of this year, which has totaled $12.2 billion so far, already twice the amount for all of 2013. Interestingly, China and the USA had equal amounts of this activity (5 out of the top ten deals), compared to last year when China dominated with 9 out of the top 10 deals. Still, Asia is the biggest driver of mobile revenue growth, and Digi-Capital projects that Asia and Europe combined could be more than 80 percent of the total revenue for mobile and online games combined.

There are two very clear messages in this report: Mobile games are going to be the leading segment of the industry very soon, and Asia is the region with the highest growth potential. Any major player’s strategy has to be measured against those two factors, and companies that lack a major effort in both of those areas will likely be falling behind the competition.