The iTunes, App Store and Google Play have over 600,000 apps each and Apple in particular says they have paid out more than $5.5 billion to developers since the launch of the App Store. With high adoption of iOS and Android devices and easy access for developers, its a great environment on both platforms.

“In particular, iOS and Android have made it possible for independent developers and mobile app start-ups to thrive,” writes Flurry’s Peter Farago. “As industries mature, however, we expect established players and brands to invade from other platforms, depressing opportunities for many early entrants. Along with this, we expect to see market revenue concentrate among fewer larger players. For this report, with these typical patterns in mind, Flurry modeled worldwide mobile app revenue, revenue sources and revenue concentration among top-ranked mobile apps on iOS and Android. For this report, we used data from over 200,000 mobile applications in the Flurry Analytics data set. Let’s start with market growth.”

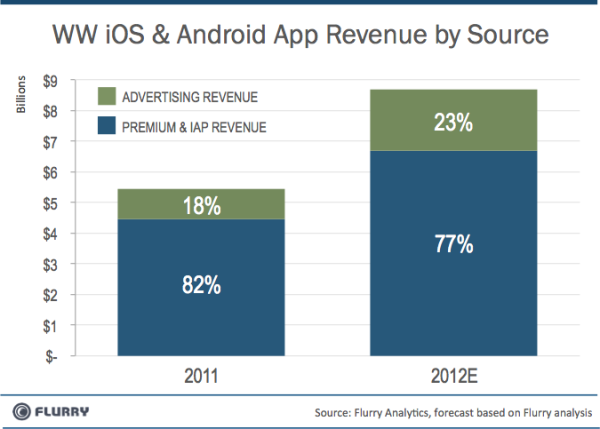

In 2012, Flurry forecasts that mobile revenue will grow by 60 percent over the previous year, reaching $8.7 billion and advertising is the fastest expanding revenue category with growth forecasted at more than 100 percent, from $980 million in 2011 to $2 billion in 2012 for 23 percent of 2012 total revenue. Likewise, premium and in-app purchase revenue is increasing at a rate of 50 percent, from $4.5 billion in 2011 to $6.7 billion in 2012.

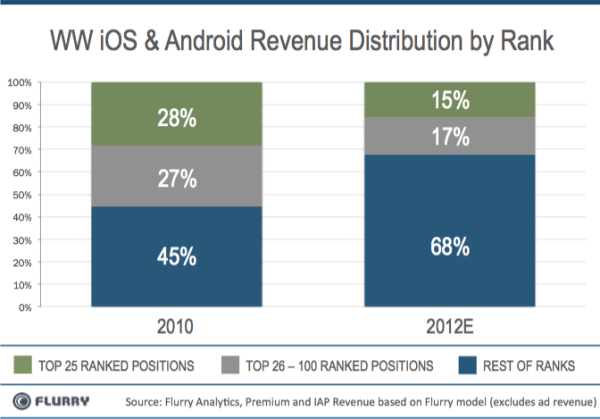

“Next, we look at the concentration of revenue among top ranked apps from 2010 to 2012. Please note that for this analysis, we focus on premium and in-app revenue only, excluding ad revenue,” noted Farago. “Comparing these two years shows how dramatically the distribution of revenue is shifting across the long tail. Starting on the left, in 2010, the green part of the column shows that 28 percent of revenue was generated by the Top 25 ranked titles on iOS and Android. In 2012, we estimate that the Top 25 will drop to commanding about half of total revenue, or 15 percent. Likewise, comparing the gray sections of each column, the rest of the Top 100 apps will drop from earning 27 percent of revenue in 2010 to 17 percent of revenue in 2012. Conversely, revenue generated by the long tail significantly grows from 2010 to 2012. Comparing the blue sections, any apps ranked beyond the top 100, we observe that long tail revenue explodes from earning under half of all premium and in-app purchase revenue in 2010 to over two-thirds in 2012.”

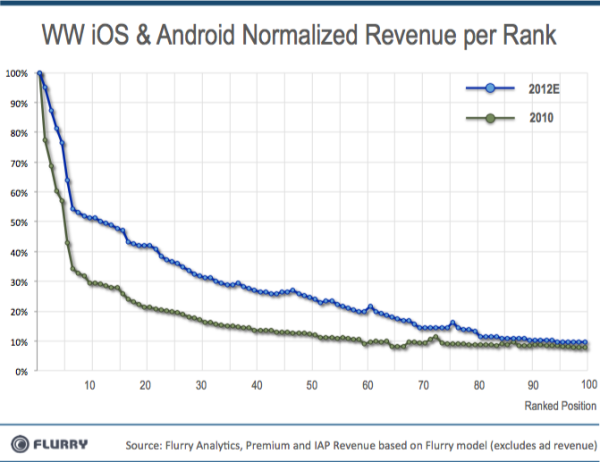

For the top 100 positions across the iTunes App Store and Google Play, relatively speaking, ranking number 50 generates more relative revenue in 2012 versus 2010. It also shows that lower level developers are doing better now than two years ago.

“With the app economy booming, companies like Facebook, Twitter and Zynga are under tremendous pressure from investors to seize the opportunity presented by this new platform. However, with software delivered in the form of downloadable applications, unguaranteed network connectivity, different consumer behavior and control exerted by platform providers such as Apple and Google, the mobile app landscape creates different, meaningful challenges for companies attempting to enter the app space from other platforms. Combined with a marketplace that reduces the power of brand recognition (e.g., apps are free for consumers to try risk free), market wealth unexpectedly continues to shift to the long tail, funding continued R&D, advertising budgets and other activities that increase their competitive strength. The age of middle-class app developer has arrived. In this economy not only are the rich getting richer, but so too are the poor, and gaining on the rich,” concludes Farago.

Source: Blog.Flurry.com