By David Cole and Steve Fowler

At the [a]list summit in February, keynote speaker Michael Pachter took exception with an observation by DFC Intelligence president and principal analyst David Cole. Cole’s statement that there is a “bubble” in social games was used in the summit’s opening address, presented by your co-author of this piece Steve Fowler.

“I think David Cole said something that’s wrong,” Pachter, research analyst at Wedbush Securities, told summit attendees. “He said there could be a social bubble, because all the games are copycat, there’s no originality… you could absolutely say that about first-person shooters. You could. They’re all the same game. Except they’re not. I would say that about Hidden Chronicles and Gardens of Time.”

“I love Zynga games and I get why they’re doing them,” Pachter continued, then followed with a double-edged compliment, “Zynga actually does a great job with their games. Even when they rip somebody off, they do a better job than the person they ripped off.”

That’s one quote that Zynga probably won’t be using in their marketing materials.

(Watch the video clip of Pachter’s keynote: http://www.youtube.com/watch v=4cgqdc1tikg) {video no longer available}

That was February 23 of this year. At that time Zynga stock was trading at $12.80 and on its way to an all-time high of $14.69 one week later. Cole looked a bit over matched by the Wedbush analyst.

Fast forward to today and it is a whole different story. As of this writing, Zynga is trading under $3.00.

What did your other co-author, Cole, see coming that Pachter didn’t?

Suffice it to say, this piece isn’t going to be a long dissertation for who was right and who was wrong. We’re going to explore the reasons for Zynga’s slide, whether they can dig themselves out, and whether they are, were or ever will be the model for Publisher 2.0.

What Zynga created on Facebook was a new distribution channel for games, but they did not create a new type of game. The game mechanics of Zynga games had been around in strategy, simulation and role-playing games. What Zynga added was a virtual item business model based on free-to-play games, and one that leveraged the communication power of social networks to rapidly bring in users.

An immediate apparent problem for Zynga was that their games were not strong at maintaining the users they brought in. Retaining users for an extended period of time is a critical component of success in the free-to-play market. By the time Zynga filed for an IPO, its prospectus made clear that the numbers did not look good for long term success.

But why didn’t Zynga’s games have staying power? Is the entire social network game category dead? If it’s not dead what needs to be done to correct it?

At DFC Intelligence, the belief is that Zynga did some very specific things that were not conducive to long term viability. Some companies are likely to learn lessons from Zynga’s experience that allow them to “reinvent” social network games and grow the overall category. This is much like what occurred after the video game bust of the mid-1980s.

The Atari 2600 pioneered a cartridge based business model where they sold a game console and made money from consumers buying expensive individual games for that console. This created the modern video game industry in the late 1970s and early 1980s. However, by 1985, the game industry was all but dead because game companies focused on throwing 1,000s of poorly conceived products at consumers. Consumers got frustrated and left many products sitting on shelves. Retailers abandoned the industry under the belief that video games were a fad that had come and gone.

Clearly video games were not a fad, and Nintendo revived the retail cartridge model in the late 1980s. Ironically, it was characters from Donkey Kong, an old game from 1981, which Nintendo used to rebuild the market. Nintendo clearly understood the power of branding, and their iconic characters such as Mario and Donkey Kong brought consumers to Nintendo in droves. They continue to do so decades later. To be fair, Nintendo does make some of the best games, but the secret to their continuous 25-year success (despite notable ups and downs) in the turbulent game industry has been mainly because of their understanding of the importance of branding and marketing. This is something that has clearly been missing on most social network games to date.

Video game consumers are passionate about their brands. The secret to building a long-term business in this industry has been all about building a popular branded franchise over years. Products that keep a solid portion of existing users while steadily adding new users are generally the ones to bet on.

Zynga’s approach has been in sharp contrast to the tried and true method for video game success. As the pioneer of a new distribution channel, Zynga, with the help of Facebook, was able to control the channel and lock out many other would be players. However, Zynga has struggled to capture loyal users for their individual products. Long before its IPO, it seemed clear their pioneering days were over and it was obvious that unless the company could reinvent itself, it was done. As one misstep, it seems easy access to data in their digital games drove them towards analytics as a more important metric than brand affinity. It’s a pitfall we covered here in our second “Publisher 2.0″ article, where digital game companies can get caught up in the race to the bottom in their cost per acquisition (CPA).

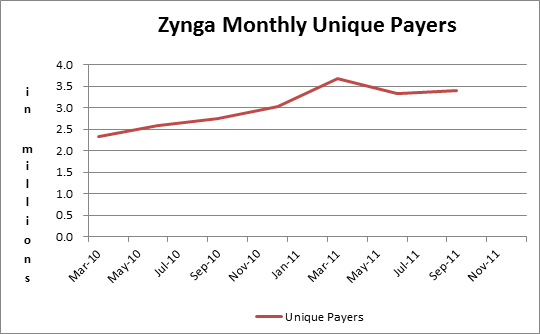

A knowledgeable person looking at the Zynga prospectus should have seen all kinds of warning signs. Revenues were soaring for 2011, and the average revenue per active user had increased from $1.01 in the fourth quarter of 2010 to $1.35 in the latest quarter (September 30, 2011 in the prospectus). The revenue per unique payer also had shown a nice increase. On the surface things looked good. However, a deeper look should have raised red flags.

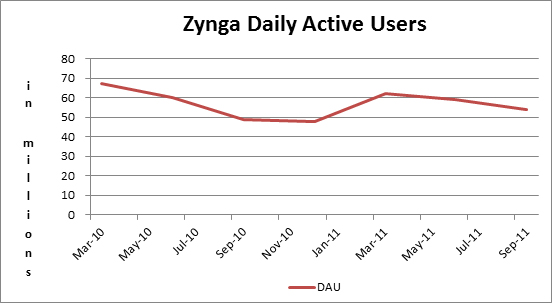

First, the overall number of daily active users was stagnant and the number of unique payers also appeared to be leveling off.

More trouble signs in the prospectus were shown in some of the big games the company highlighted, most notably FarmVille, FrontierVille and CityVille. Zynga noted that FarmVille had 32 million monthly active users and FrontierVille had 11 million. However, this was down substantially from the start of 2011 when the former stood at 54 million and the latter was at about 30 million. CityVille, which launched at the end of 2010, was the star at the time with 61 million monthly active users but this was down from a peak of nearly 100 million users in early 2011.

Based on user trends alone, this looked like a bubble ready to burst. And looking at the supply side of the equation also raised alarming trends.

In 2011, Zynga did a great job of solidifying its solid leadership position on Facebook. But Facebook had just started its Facebook Credits program and was getting ready for its own IPO. Clearly Zynga was locked into Facebook as its distribution channel. It’s always a warning sign when a content publisher is dependent on a single distribution channel it cannot control.

There was also growing competition from companies developing better Facebook games as well as new platforms including both other social networks and emerging ones such as mobile. Zynga claimed that they would build their own game-focused social network outside of Facebook, put effort towards making major improvements in game quality, and turn their attention to mobile platforms in a major way. However, these were all serious challenges, ones where it was uncertain if the company’s one successful endeavor on Facebook would give them any advantage. One thing was certain, that it would be expensive for Zynga to pull it off.

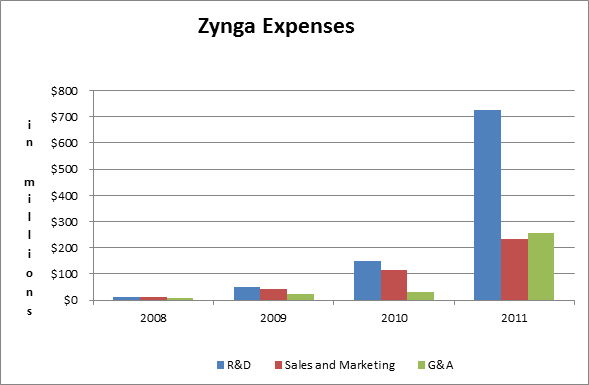

Zynga expenses were already starting to soar at the time of their IPO, and they only continued to do so into 2010. Research and development costs for 2011 were up 385 percent, while marketing costs doubled. Arguably this might be expected from a company growing so fast. However for the first six months of 2012, research and development costs were up 114 percent while revenue from online games was increasing at an anemic 18 percent. Furthermore it doesn’t appear that revenue growth came from more efficient marketing, as sales and marketing costs were up 45 percent.

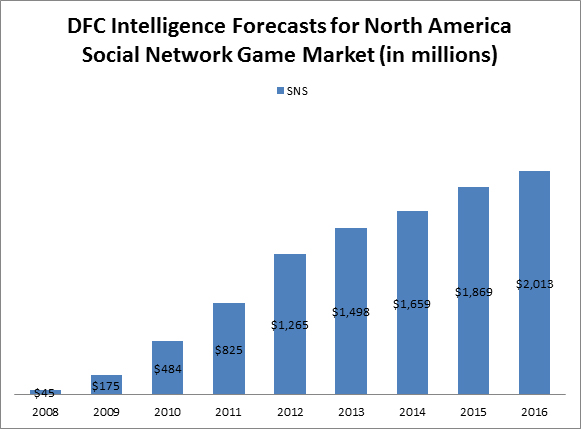

The fact that Zynga is struggling has many people assuming the concept behind games on social networks is flawed. This is throwing the baby out with the bathwater. DFC’s belief is that games delivered via some form of social network will have strong growth potential. In North America, DFC sees the market doubling to more than $2 billion by 2016. It just doesn’t necessarily mean that growth will come from Zynga and Facebook.

It is important to look closely at Japan, where in-app purchases of games using social networks have boomed in the past two years. Trends in gaming in Japan are often precursors to trends in North America and Europe. This has been true for both major game platforms and many mass market casual game trends.

In DFC’s recently published report “The Secret of Gree & Mobile’s Success” {link no longer active} there is a detailed look at trends in in-app purchases via social networks. This report notes that there is a big difference between social networks and how well they do with gamers. Mobage and Gree had less than half the overall users of other social networks such as Facebook, Twitter and mixi, Japan’s most popular social network. Yet they attract an audience that is dedicated to games. Gree and Mobage attract a higher percentage of paying users, and their paying users spend more on average.

Mainly from delivering virtual item-driven games to Japanese consumers, Gree and DeNA, Mobage’s parent company, are both on track to reach $2 billion in annual revenue. At the very least, these companies have proven that a big market is out there. While both Gree and Mobage face many of the same challenges of Zynga, including market saturation, there is no doubt that they were able to tap into demand that generated a huge new source of revenue by getting consumers to spend money in new ways. Most importantly, they show that Facebook may not be the ideal social network for gamers. In fact, DFC believes that specialized social networks will become a big growth area, especially for games.

A big issue with both Zynga and Facebook is that they targeted raw user numbers instead of looking for quality of users. The Zynga IPO came right at the time of Nexon’s IPO in Japan. Nexon is a Korean free-to-play game maker and distributor that, on the surface, looks similar to Zynga. The companies are extremely different. Nexon focuses on building a loyal long-term user base that plays its games for years. Nexon also focuses heavily on quality over quantity, and is heavily into branding its games.

Nexon and Zynga had an IPO at the same time, and they both had very similar revenue for 2011 at about $1.1 billion. The difference was Zynga was much newer, and thus in theory on a faster growth track. However, looking at Nexon’s prospectus of late 2011, there were stark contrasts, most notably in the Nexon’s much smaller portfolio and the longevity of its games. Nexon was focusing on quality over quantity. They presented games such as MapleStory, which launched in 2003, and Dungeon Fighter, which launched in 2004. Both had their best revenue year in 2010, with $1.5 billion in cumulative revenue each. Other games such as Mabinogi and Counter Strike Online were also having their best years several years after launch. Since its IPO, Nexon’s stock has been somewhat volatile, but it is generally traded near or above its IPO price. It’s a very different story from Zynga.

Zynga is now looking into growing its business on mobile platforms. Of course, pioneering the mobile market in Japan was a big secret behind Gree and Mobage’s success. The issue is whether the pioneering days are over.

While mobile games may be a growing area, it is worth looking at whether Zynga can crack a market that is already tremendously overcrowded and dominated by small, lean players. There is also an issue of player fatigue around the entire Zynga game type, and moving to mobile is not likely to change that. On the other side, Gree and Mobage in Japan show that in-app purchases on mobile platforms can be done. This does not mean Zynga will be the one to do it, considering they do not have a first mover advantage in mobile.

The issue with Zynga products is that, first, they quickly reach the saturation danger point, and second, the company doesn’t support building strong brand loyalty among its core users. Brand loyalty is the key to long-term success in all aspects of the game industry. As mentioned, strong branding and high quality were critical for Nintendo. The same can be said for most successful companies in the game industry. Examples abound, with EA’s sports franchises and products such as The Sims, Activision-Blizzard’s Call of Duty and Warcraft IP, and the many Japanese publishers that are still doing well off of franchises from the 1980s. Branding is crucial, and not just for core games. It is also the secret to success with casual games. PopCap is a perfect example of a company focused on branding with products such as Bejeweled and Plants vs. Zombies. It’s a major reason EA paid about $750 million for PopCap in 2011.

Branding is a long term commitment that requires careful management of a franchise. The game industry has numerous examples of game fads that quickly burned out, often due to oversaturation. Even strong brands can’t escape saturation and player fatigue. Activision’s Tony Hawk and Guitar Hero franchises are examples of that. EA Sports is one of the few examples of where a franchise can be continually pumped out, mainly because of the loyalty to the underlying sport. Even with the incredibly popular Call of Duty there is an issue of how many games Activision will be able to pump out before there are diminishing returns. Meanwhile, a company like Blizzard whose inability to pump out quick sequels to WarCraft, StarCraft and Diablo may in fact help maintain the brands demand over time.

The problem with Zynga is they seem to have quickly hit the saturation danger point, when too many essentially similar titles in essentially similar genres generate decreasing returns. A FarmVille begets a CityVille begets a FrontierVille, but the attachment consumers form with each succeeding and very similar game is weaker and shorter in duration.

Once again, there are many historical trends of this occurring in the game industry, even among core gamers. In the late 1990s, there was a boom in real-time strategy (RTS) games that quickly led to a flood of new products. What eventually happened was that even the best new entries in the genre had fewer users, as they were all targeting a subset of the established user base. There was a declining percentage of gamers willing to make the jump from Command & Conquer to Dark Reign to Warzone 2100, or from Age of Empires to Total War to Empire Earth to Rise of Nations.

Zynga also faces the challenge of competing with the thousands of simple free-to-play games on one hand, and the more robust games on the other hand. The company built its audience on gamers looking for a quick, simple experience. Now, to get more heavy paying users, Zynga is trying to make its games more complex.

An article in Kotaku has some excellent points about how the typical Zynga player liked how simple games like FarmVille were to play. But as the games got more complex, the masses churned faster. There will always be a certain percentage of game players turned off by added complexity. Of course, much of Zynga’s goal may have been weeding out those users in an effort to attract more robust paying users. The issue is many experienced gamers looking for interesting challenges don’t look to “Blank-Ville” games because they are frustratingly slow if you don’t pay. If they are going to pay, they will opt to pay for something more interesting. Meanwhile, the typical “Blank-Ville” gamer who grew with the complexity of each new game might eventually recognize that the games are still basically the same, leading to burnout.

Clearly, Zynga is looking to build both game quality and focus on building stronger brand recognition. Much of this is following in the example of Rovio’s Angry Birds as an impressive case study for successful branding. In late 2011, Zynga partnered with Best Buy to release plush toys based on FarmVille that came with in-game credits. In early 2012, Zynga announced a partnership with Hasbro to make, among other things, a CityVille branded version of Monopoly, a FarmVille themed version of the classic board game Hungry Hungry Hippos, a Word with Friends board game (essentially a different branded version of Scrabble), and probably a Pictionary themed game based on Draw Something. These products are due in October for the 2012 holiday season.

Zynga wants to build more of a presence for its brands, but the deals with Best Buy and Hasbro are fairly limited efforts. The plush toys at Best Buy were more of a minor test, and monthly active users of FarmVille on Facebook have declined from about 31 million in December 2011 to only 18 million in August 2012. The Hungry Hungry Hippos board game is targeted for a 6 year-olds and under audience, not really the audience for FarmVille. Monopoly, Scrabble and Pictionary are well-established board games, but they seem to have reached their own saturation point.

In the end, Hasbro may be the one to benefit the most from the association by attracting Zynga users. It seems doubtful that these products will bring in many new users to Zynga games. At best, they are probably a minor upsell for serious Zynga users.

Can Zynga be saved?

That question is out of our hands. Recent marketing efforts are not positive. If we look to a positive sign, it is the significant increase in R&D that is worrisome but could be a potential source of salvation. Zynga is a company that has lived on success in days and months, but R&D pays off in years. It comes down whether their R&D money is being well spent, and whether their investors have the patience to see it bear fruit.

Source for all data: DFC Intelligence (www.dfcint.com)

—

This is part of a series of articles for [a]list daily outlining the changing face of publishing and marketing games on digital platforms. Previous articles include “Why Publisher 2.0 is M.I.A.” Part 1, looking at the changing face of game publishing, and Part 2, the shift in digital games from marketing a product to marketing a service, along with “The Emergence of Mid-Core,” a piece co-authored with Peter Warman, head of analyst firm Newzoo, “Riot and the Rise of the Player Community,” an interview with Riot Games, and “Finding Publisher 2.0,” an interview with Wizards of the Coast.