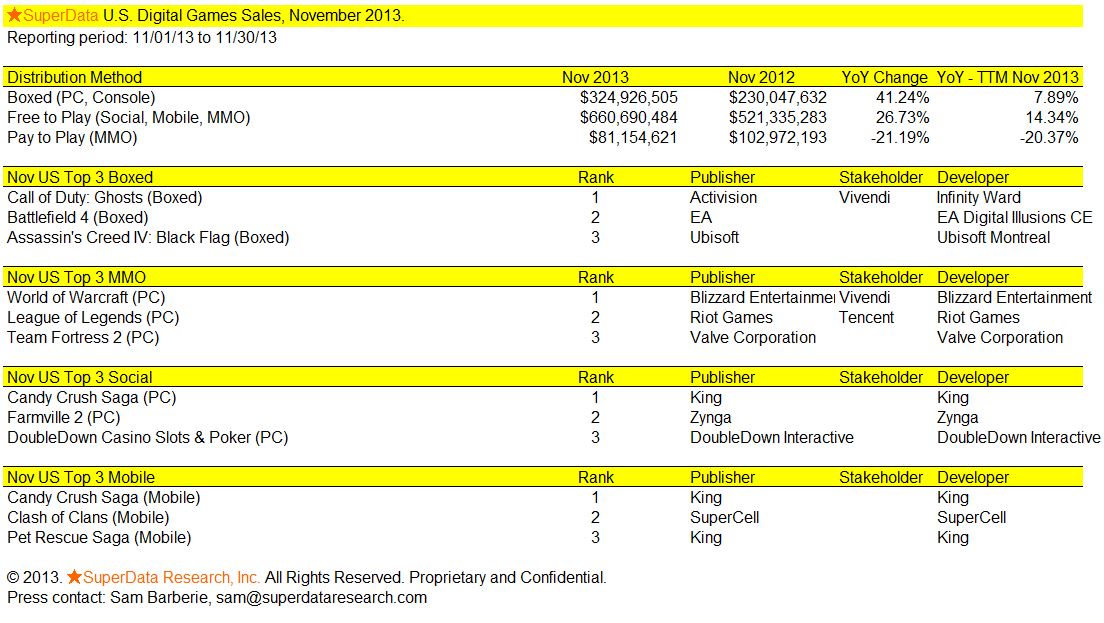

The combined digital games market totaled $1,066 million in sales in November, up 25 percent compared to November last year. November sales figures were a testament to the continued importance of retail game sales, as a 31 percent month-over-month spike in the PC and console DLC segment, reaching $325 million in sales, offset a 17 percent decline in free-to-play. A year ago, the combined sales for PC and console DLC totaled $230 million. The social and mobile game categories grew by a few percentage points month-over-month, even as its top earners show no sign of weakness.

Social Games

- Social games totaled $169 million in November, as the conversion rates across genres improved. This is consistent with our previous anticipation of a slight decline prior to the end of the year. We maintain that, based on seasonal patterns and the recent strengthening of the segment, total spending may break the $200 million threshold in December.

- Criminal Case (Pretty Simple Games) reached a milestone of 100 million lifetime players, and the success of the overall hidden object genre also persists. Zynga’s Hidden Shadows is currently among the top trending titles in the category, and Game Insight released Hotel Enigma this month, hoping to emulate the success of its predecessor Mystery Manor.

- By all accounts, Facebook is now a saturated gaming platform. King’s dominance of the top charts in social — with Candy Crush Saga, Pet Rescue Saga and Farm Heroes Saga totaling an estimated 75 million daily actives — other publishers are forced to search for greener pastures. Successful studios like Ironhide Game Studio announced the release of its popular Kingdom Rush: Frontier, a tower defense-style game, on free online game site Armor Games.

Free-To-Play MMO

- The free-to-play category showed a significant drop in November, declining 17 percent month-over-month, totaling $217 million in sales. The overall size of the audience remained stable at around 45 million monthly actives, but the average spend per user declined 10percent month-over-month. The release of several big, blockbuster titles at retail succeeded in claiming an above average share of monthly spending among this dedicated gamer audience.

- Hoping to repeat the success of its World of Tanks, which generated an estimated $1 million in daily revenues in November, Wargaming released World of Warplanes on November 13. The free-to-play flight combat game offers 15 vs 15 player sessions, and its in-game economy connects to World of Tanks via a Unified Account System. On the same day of its release, publisher Gaijin Entertainment announced the December start of closed beta testing of War Thunder: Ground Forces, a direct rival to World of Tanks, and released aerial combat game War Thunder as a free-to-download game on PlayStation 4. World of Tanks, which has been in beta on the Xbox 360 since earlier this year, is part of Wargaming’s effort to penetrate the U.S. market and become the biggest free-to-play title on a console.

- Other highlights in the free-to-play MMO space include Trion Worlds announcing Trove, a voxel-based procedural world that resembles Minecraft (Mojang), Roblox (Roblox Corporation) and Cube World (Picroma) and a performance patch for PlanetSide 2 (Sony Online Entertainment), which greatly improves the average frame rates. Blizzard offered a slew of announcements including the open beta for online trading card game Hearthstone (Blizzard) starting in December, followed by an iOS version mid-2014. Its Heroes of the Storm will move into beta”soonish…er” and StarCraft 2 Arcade Mode will be available as free-to-play.

Pay-To-Play MMO

- Overall earnings for subscription-based MMOs declined in November, totaling $81 million in revenues, as the overall user base lost another 400,000 subscribers. For the remainder of the year, we anticipate a further decline during the holiday season with the release of the next console generation and accompanying titles.

- On a title level, most subscription-based MMOs showed a slight month-over-month decline, and recorded only minor subscriber churn. Big winner in November was Lord of the Rings Online which, after suffering a power outage, released its Helm’s Deep expansion two days late but still managed to add about 80,000 new players to its user base, totaling just under 400,000 subscribers.

Mobile

- After a slowdown, the mobile games segment regained momentum in November, growing 4percent month-over-month, and reached $274 million in total sales. Compared to the same month last year, total mobile game spending has increased 34 percent.

- Despite receiving a lot of additional marketing momentum from Apple, Natural Motion’s Clumsy Ninja failed to claim a top tier slot immediately after launch. Instead, incumbents King and Supercell prevailed. According to industry sources, both publishers have been aggressively buying up users, not in an effort to both expand their customer base but rather to shut out any competitors.

- After we recorded two casino-style games among the top five grossing in October, both DoubleDown Casino (IGT) and BigFish Casino (BigFish) slid down the rankings in November. Machine Zone’s Game of War: Fire Age continues to do well, claiming the number 4 spot among top earners in November with an estimated $460,000 in daily revenues.

Downloadable (PC + console)

- A host of new releases in November triggered a spike in spending on, especially, console DLC. Combined with PC, the DLC segment totaled $325 million in sales in November, up 41 percent from November last year.

- Several big franchises released on the same day as the next gen consoles. In particular Call of Duty: Ghosts, which generally launches two months later, was now immediately available via digital download on Xbox Marketplace and PSN. Similarly, Need for Speed Rivals and the late-October release of Assassin’s Creed: Black Flag and Battlefield 4 drove overall sales. We expect this trend to continue for the remainder of the year.

About this monthly release

In an effort to help create greater transparency in the digital games space, SuperData provides a high-level overview of the U.S. market every month. Our methodology builds on digital point-of-sale data collected directly from publishers and developers.